Our take on the latest Economic and fiscal update (Thu 22 May 2025)

Core crown revenue down $9.8b, and expenses down $3.1b

Return to surplus in 2028/29

Investment Boost tax incentive to drive investment

The key numbers...

- Slow economic conditions are highlighted in Budget 2025, with a focus on weaker growth from trading partners. New Zealand’s softer outlook for economic growth contributes to a $9.8b reduction in forecast Crown revenue between 2025 and 2029, compared to expectations in December’s Half Year Economic and Fiscal Update (HYEFU).

- Tighter restraint on spending comes through a $3.1b reduction in core Crown expenses over the same period. Lower spending, along with the recovering economy, narrows spending from 33.0% of GDP in 2024 to 30.9% of GDP in 2029, but expenses will still be above the pre-pandemic level of 28% recorded in 2019.

- The combination of lower revenue and reduced spending results in the operating balance before gains and losses excluding ACC (OBEGALx) still being forecast to turn from deficit to surplus in 2028/29, although the expected surplus in that year has shrunk from $1.9b to $0.2b.

- The Investment Boost tax incentive scheme will allow businesses to deduct 20% of the cost of new machinery, tools, and equipment from their taxable income. This policy is aimed at driving investment in assets that underpin productivity and output growth. This policy is expected to drive a total 1% increase in GDP over the next 20 years, with half of that increase coming over the next five years.

- Budget 2025 helps clear up some uncertainty over public sector non-residential building. A billion-dollar allocation to investment in hospitals was announced, targeting the major redevelopment of Nelson Hospital. The package also includes construction of a new emergency department at Wellington Regional Hospital, remediation work at Palmerston North Hospital, and critical Auckland Hospital infrastructure. There is also scope for more education building, with $712m of capital and $234m of operating spending for new classrooms and school property. At the moment, however, there remains a gap between funding and actual activity, with a lack of work in the pipeline, let alone shovels in the ground and works underway in the construction sector.

- KiwiSaver changes were signalled to come through in this year’s Budget. The default employer and employee KiwiSaver contribution rates will increase from 3% to 3.5% from April 2026, and then to 4.0% two years later. Changes are coming to the government contribution rate, with the maximum contribution being cut by 50%, to $260.72 per year. This annual government contribution will also only be available to people earning $180,000 or less.

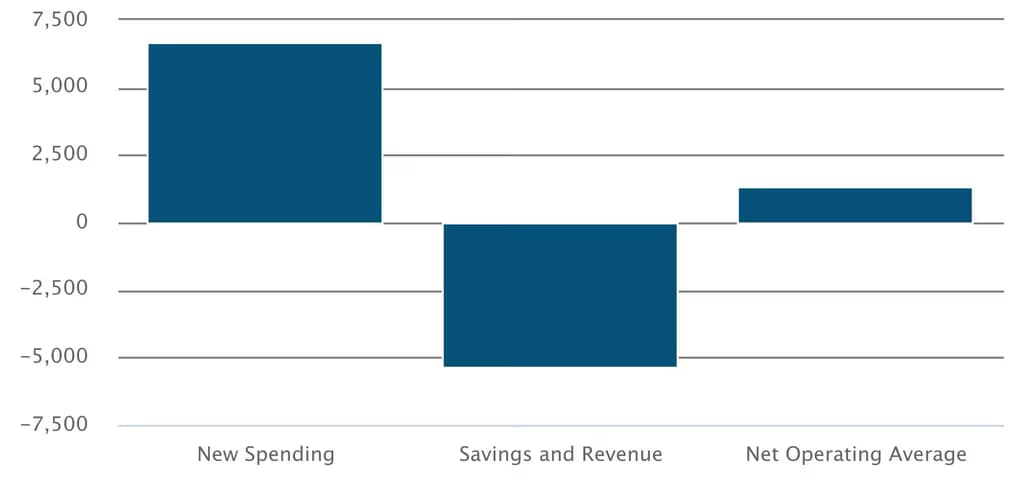

Lowest net new operating spending in a decade

Budget 2025 Package ($m)

...and our reaction

- The 2025 Budget focuses on making savings in some areas and switching that spending to fund new initiatives. Changes to Working for Families, raising the income threshold to support low- and middle-income families, but also increasing the abatement rate, demonstrates a reprioritisation of spending. Cuts to KiwiSaver contributions will hit households’ retirement savings, with that government money reprioritised to different areas.

- Health and housing were a focus of the budget, with a $7b increase in funds to deliver health services. New funding of $128m over four years aims to deliver at least 550 more social houses in Auckland in 2025/26, in addition to the 1,500 new social houses funded through Budget 2024.

- There were additional funds for investment in infrastructure, with $605m for capital and operating rail maintenance, to replace bridges and other assets and increase the reliability of services for commuters and freight operations in Auckland and Wellington. There was also $219m in additional operating funding for local roads damaged by North Island weather events in 2023.

- The forecast 2025/26 NZ Government Bond programme has been reduced by $2b from what was set out in HYEFU 24, down to $38b. Net core crown debt is set to peak at $128b in 2027/28, bringing the peak forward a year from the previous forecast of $129b in 2028/29.

- Despite the introduction of the Investment Boost tax incentive, business investment is set to grow more slowly over the forecast period, with average growth revised down to 3.6%pa between 2025 and 2029, compared to a forecast of 3.8%pa in HYEFU 2024. Although investment is lower than previously forecast, this weaker growth is due to near-term uncertainty from global trade events. Forecast investment is higher than it would be under the baseline scenario, without the Investment Boost tax incentive.

Latest updates

Premium

Economic and fiscal update

Budget 2026: Fiscal position set to improve

Thu 28 May 2026

Premium

Economic and fiscal update

OBEGALx return to surplus delayed yet again

Tue 16 Dec 2025

Economic and fiscal update

Return to surplus pushed out another two years

Tue 17 Dec 2024