Our take on the latest Monetary policy review (Mon 23 Mar 2020)

RBNZ to buy $30b of government bonds

Aim is to bring down longer-term interest rates

Government to underwrite lending to affected businesses and mortgage holders

The key numbers...

- The Reserve Bank's Monetary Policy Committee has authorised the Bank to buy up to $30b in government bonds over the next year.

- The Committee determined the economy needed additional support given rapidly deteriorating economic conditions.

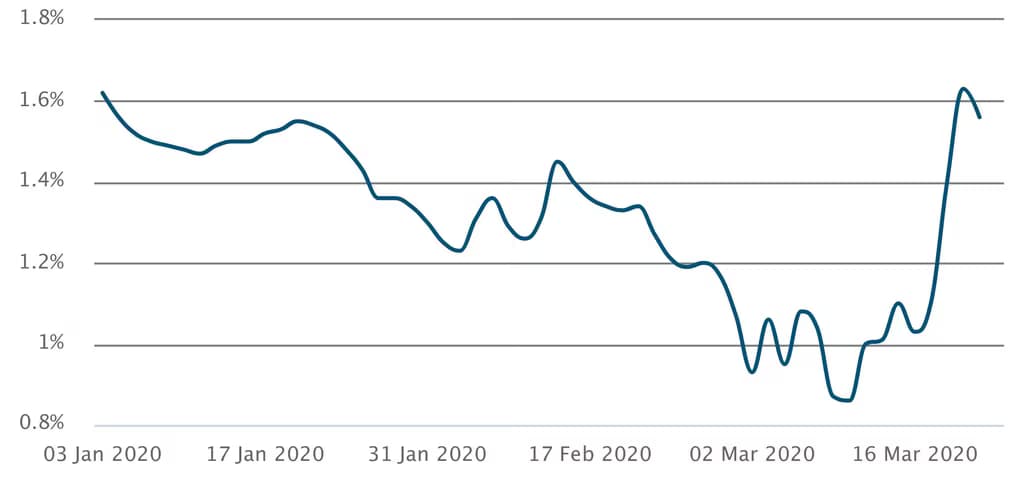

- The Bank noted that “heightened risk aversion has caused a rise in interest rates on long-term New Zealand government bonds and the cost of bank funding” – 10-year bond rates jumped 60 basis points between Monday and Thursday last week.

- The Bank is beginning with bond purchases of $750m per week on the secondary market, looking to “front-load” its efforts to support the economy.

- The Government has also announced an agreement with retail banks and the Reserve Bank to guarantee lending to businesses that would otherwise be viable but have been affected by COVID-19, as well as providing support for mortgage holders where necessary.

Ten-year government bond rates

...and our reaction

- Higher long-term interest rates at this stage of the crisis are unhelpful, pushing up bank funding costs and debt-servicing costs for businesses at the same time as many firms will be experiencing a drop in revenue and, consequently, cashflow issues.

- The Reserve Bank is not aiming to reduce the government’s financing costs in the face of increasing government spending and rising debt levels, although this outcome is a side-effect of the Bank’s actions to bring down interest rates.

- Bond purchases of $30b represent approximately 40% of the government’s current debt, which is the maximum the Bank believes it can purchase without reducing liquidity in the market and unduly influencing interest rates.

- Future increases in government debt could create scope for the Bank to increase its total bond purchases, although any lift from the current cap of $30b would represent additional quantitative easing and so would require an additional mandate from the Monetary Policy Committee.

- The Reserve Bank is not clear at this stage what its next support measure for the economy would be, but it has ruled out a negative official cash rate (OCR), and it is also unlikely to purchase interest rate swaps (which are a key factor determining fixed mortgage rates, but they are currently consistent with the Bank’s forward guidance for the OCR).

Latest updates

Premium

Monetary policy review

Reserve Bank holds at 2.25%, but watches vigilantly

Wed 8 Apr 2026

Premium

Monetary policy review

OCR on hold, but set to lift slightly quicker

Wed 18 Feb 2026

Monetary policy review

OCR cut to 2.25% looks like the last

Wed 26 Nov 2025

Monetary policy review

OCR down to 2.5% as RBNZ cuts big

Wed 8 Oct 2025